Part 2 of a 3‑part investor series

In Part 1 of this series introduced U.S. Energy Corp. (NASDAQ:USEG) as a company undergoing a strategic transformation, then Part 2 marks the point where that transformation becomes visible.

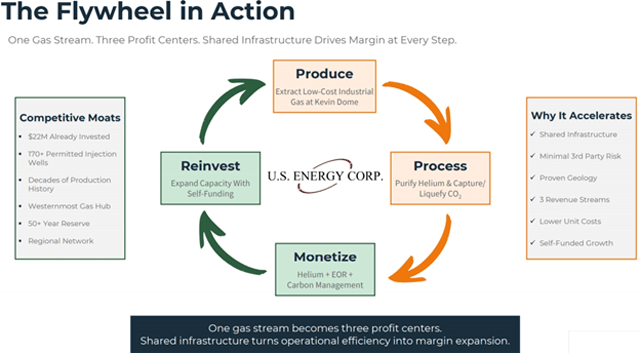

2026 is a pivotal year—not just because of what U.S. Energy plans to build, but because of what that buildout enables: a fully integrated industrial gas and carbon management hub capable of delivering multi‑stream revenues for decades.

This is the moment when the vision becomes infrastructure, and when Kevin Dome begins evolving from geological resource into economic engine.

The processing facility: Where the platform comes to life

At the centre of the 2026 plan is the company’s planned processing facility, a purpose‑built complex designed to handle roughly 8 million cubic feet per day of inlet capacity. While the number itself tells one part of the story, the real significance lies in what that capacity produces—and how it integrates with the rest of U.S. Energy’s assets.

Inside this facility, raw gas drawn from the Kevin Dome will be separated into two commercially powerful outputs: high‑purity helium and refined CO₂, each with its own market, its own set of buyers, and its own strategic purpose within the company’s broader platform.

To support continuous, industrial‑scale operations, the facility is expected to require approximately 2.5 megawatts of power, sourced primarily from the regional electrical grid. Backup power will come from U.S. Energy’s own natural gas infrastructure—a not‑so‑subtle reminder of why integrated ownership matters in real‑world operations. It’s not just about extracting gas; it’s about controlling the ecosystem that keeps the entire value chain running.

Once operational, this facility becomes the beating heart of the entire platform.

Building the arteries: The 2026 infrastructure program

Spring 2026 will mark the start of a critical phase in Kevin Dome’s development: the installation of roughly 10 miles of in‑field gathering pipelines that will move produced gas from the company’s existing wells to the processing plant. The timing has been structured deliberately, with construction scheduled to finish in the third quarter of 2026—just ahead of anticipated commissioning and first operations.

This is the kind of infrastructure that doesn’t make headlines, but it defines scalability. It transforms resource potential into operational reliability, and operational reliability into bankable value. By the end of 2026, U.S. Energy expects to have the core midstream backbone in place, enabling long‑term industrial gas production, CO₂ management, and enhanced oil recovery at commercial scale.

Regulatory advantage: First in Montana, and among the largest in the nation

While steel in the ground matters, regulatory positioning often determines which companies thrive and which fall behind. In this area, U.S. Energy has distinguished itself early.

The company’s submission of two Monitoring, Reporting, and Verification (MRV) plans to the U.S. Environmental Protection Agency—covering its Class II injection wells—represents the first MRV submissions ever made in the State of Montana. Once approved, the Kevin Dome program would rank among the 20 largest CCUS projects in the United States.

This gives U.S. Energy something far more valuable than a permit. It gives the company a defensive moat:

- A regulatory footprint that establishes leadership

- A head start in building one of the nation’s major CO₂ sequestration hubs

- Competitive separation from late‑moving peers in industrial gas and carbon management

In a sector where compliance and verification are often the biggest barriers to commercial operation, U.S. Energy is positioning itself ahead of the curve.

A resource of rare scale—and a major asset in a tightening market

Behind the 2026 buildout is the sheer magnitude of the Kevin Dome resource. After a multi‑year effort to aggregate land, U.S. Energy now controls nearly 80,000 net acres, a footprint large enough to support long‑duration development and multi‑phase expansion.

Independent evaluation has confirmed the dome contains approximately 1.3 trillion cubic feet of naturally occurring CO₂ and 2.3 billion cubic feet of helium. These numbers matter not only because of their size, but also because of what they represent: decades of feedstock for both industrial gas sales and carbon management services.

In a time when helium shortages are disrupting global semiconductor and aerospace supply chains—and when companies across the U.S. are under increasing pressure to secure long‑term CO₂ sequestration—the value of owning such a resource outright cannot be overstated.

The closed‑loop revenue model: Monetizing both sides of the molecule

Perhaps the most compelling part of the 2026 plan is how these elements come together economically. U.S. Energy is not simply extracting gas and selling it. Instead, it is creating a closed‑loop revenue model that monetizes both helium and CO₂ through distinct, synergistic pathways.

The high‑purity helium produced at the processing facility will be sold into premium markets—semiconductors, aerospace, medical technologies—buyers who depend on long‑term, reliable supply and pay accordingly.

The CO₂, meanwhile, will follow a different path: it will flow into company‑owned oil fields for enhanced oil recovery, increasing output from assets U.S. Energy already controls 100 per cent. The same CO₂ then becomes eligible for permanent geological sequestration, supporting long‑duration carbon credits and providing optionality for additional revenue streams.

In other words, the company produces two valuable gases—but keeps the CO₂ working internally to uplift another business line, all while strengthening its position in the emerging CCUS economy.

Few emerging companies offer this level of integration, resource control, and multi‑vertical monetization.

Why industrial gases are the gold of the digital age

With the 2026 plan outlined, the next chapter in this series will step back and explore the broader landscape. Why do helium and CO₂ matter so much right now? Why are industrial gases becoming essential inputs to the digital economy? And why might companies like U.S. Energy Corp. hold the key to the next era of critical‑material security?

Part 3 will examine why industrial gases are increasingly viewed as the “gold of the digital age”—and what that means for investors positioning ahead of long‑term demand.